")

: 29 Days, 60+ Museums, 50% OFF")

Last time we discussed what it’s like to first meet with a financial planner. Taralyn Rose of California Coast Credit Union discussed what she hopes to accomplish when meeting with someone for the first time, including checking credit and spending, setting goals, and assigning homework.

The second meeting looks much different from the first, and can really help put someone (or a family) on the right track to accomplishing their financial goals.

LL: When does the second meeting generally take place?

TR: I typically recommend at least a month between meetings. This gives the person enough time to thoroughly track an entire month’s expenditures and go back through their financial history to find annual costs such as car registration and membership dues.

LL: What do you want to see when someone comes in for the second meeting?

TR: The expectation is that my client has completed the monthly tracking sheet. This may seem simple but there are so many things that we don’t think about regularly. I need to see where every single penny went in that month. Even the smallest things add up over time and can have a bigger impact on a budget than you might realize.

LL: What happens once you look over the monthly tracking sheet?

TR: The biggest realization happens when we compare the predictions from the first meeting to the reality of the monthly tracking sheet. If the numbers lined up then they most likely wouldn’t be coming to see me. There are usually major differences in each category of the tracking sheet between what clients predict and what they actually spend. The single biggest difference I see is the prediction of the periodic expenses. Recognizing these inconsistencies is what sets the foundation for creating a more realistic budget and getting yourself on track to meet your financial goals.

LL: What do you consider periodic expenses?

TR: Anything that is not part of your typical monthly budget. Most people have bills like utilities, car payments, rent/mortgage, that they can accurately track. It is more difficult to predict when you need new tires, when you might need a new fridge or television, or how much you spend on gifts for birthdays or the holidays.

LL: And why do you think this is the most important aspect of expense tracking and budgeting?

TR: This is what I most frequently see charged to credit cards, and the reason why balances don’t go down as people want them to. When someone is in a financial situation where they are seeking my help, this is almost always a major factor as to why their debt is so high and they are feeling overwhelmed. It is also a great place to start the process of setting up a new budget that reduces the risk of unexpected and unaffordable financial crises arising throughout the year. That may seem impossible, but a lot of what we think is unexpected can actually be predicted by looking at what people generally need to spend money on throughout a calendar year.

LL: So what do you do next?

TR: The second meeting has three parts: Look over the expense tracking sheet, set SMART goals, and create a plan for attaining those goals. Now that we’ve compared the predictions to the reality, we can set goals. SMART means specific, measurable, attainable, relevant, and timely. The goals need to be very specific. Saying “I want to pay down my credit card debt” or “I want to save more” are not clear enough to be realistic. I want to put a figure on that, such as “I will pay down $2000 in debt in the next year” or “I want to put $2000 in my savings account in six months.” These are goals that are specific enough we can measure them. The number will change depending on the person’s situation so that it is attainable. It also must be a goal that matters to that person. Often someone will have a lot of input from friends or family, but the recommendations are not necessarily relevant to them. If the goal doesn’t matter, they are not likely to put in the effort to achieve it. Timely means we put a time frame on the goal so that they know if they make the adjustments they have set for themselves they will see the result in a specific time frame. This is very important because who wants to work at something and not be able to see an end in sight? I can tell you that if you put your money toward a specific debt, it will take a measurable amount of time to pay it off and you will be able to see that happen.

LL: How do you set these up?

TR: We use the real expenses to form a plan for each paycheck, making sure to include setting money aside for periodic and annual expenses. We look at the real numbers and talk about the SMART goals so we can make adjustments to the cash flow. We discuss where adjustments can be made in order make the spending support the goals. I can use cash the flow worksheet to see which debt makes the most sense to pay off, taking into account interest rates and monthly payments. We will write down an order of attack, making it clear which to target first, second, etcetera. I instruct them to pay the minimum on everything else in order to make the most progress. Other possibilities include analyzing whether or not someone can qualify to refinance their car to lower the payment and/or rate, take cash out if the car is paid off in order to pay off higher interest rate debt, and find credit cards with lower rates or zero interest periods that can help make their payments go further. This part can take quite some time, but it is very important. Once we are done with this my clients will have a plan that, if followed, will get them to the financial goals they have been struggling with for so long.

LL: How do you wrap things up for the second meeting?

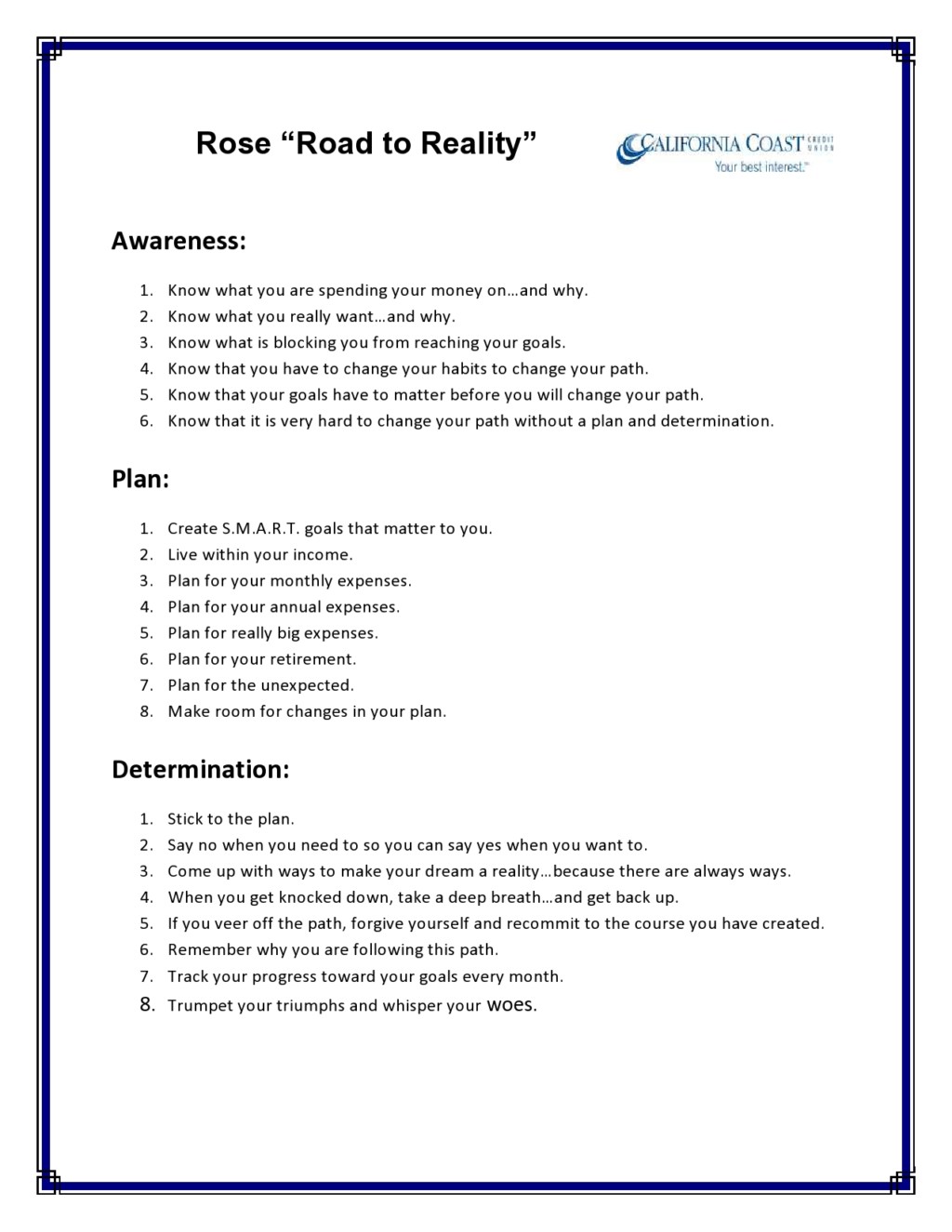

TR: At the end of our second meeting I like to make sure they know how to use the expense worksheet, including adding categories and making adjustments. We put the goals at the top so they are always visible and help keep them motivated. I also give them my Rose’s Road to Reality document which talks about the process of achieving financial goals and making the hard decisions to reach these goals. It also helps with maintenance over the coming months as they work toward the goals and prepares them for meeting number three. The homework for this meeting is to follow the plan we have set for budgeting the various expenses and to begin looking into ways to reduce other expenses. This can include shopping around for car insurance, cable and internet packages, and cell phone plans. They will leave this meeting knowing that by the third meeting I expect to see they have reduced expenses where we have determined it is possible and stuck to the plan for budgeting in the other areas.

Next time we will discuss what the third and other follow-up meetings entail and how this journey to financial fitness concludes.

Next time we will discuss what the third and other follow-up meetings entail and how this journey to financial fitness concludes.

on the right track to accomplishing their financial){kind=link}

This is very helpful. These days, we need to be financially wise, earn, save, invest and grow.